Blog

Expert perspectives on modern wealth management, platform innovation, and the technology shaping the future of financial services.

Blog

BlogAgentic AI vs. AI-Assisted Wealth Software: What's the Actual Difference?

The wealth management industry is using the word "AI" the way it once used "digital" as a signal of modernity rather than a description of what the technology actually does.

Blog

BlogRIA M&A Integration Challenges and How Agentic AI Solves Them

RIA M&A activity has not slowed down. The number of transactions hitting the market each year continues to rise, deal multiples remain competitive, and acquiring firms are under pressure to close…

Blog

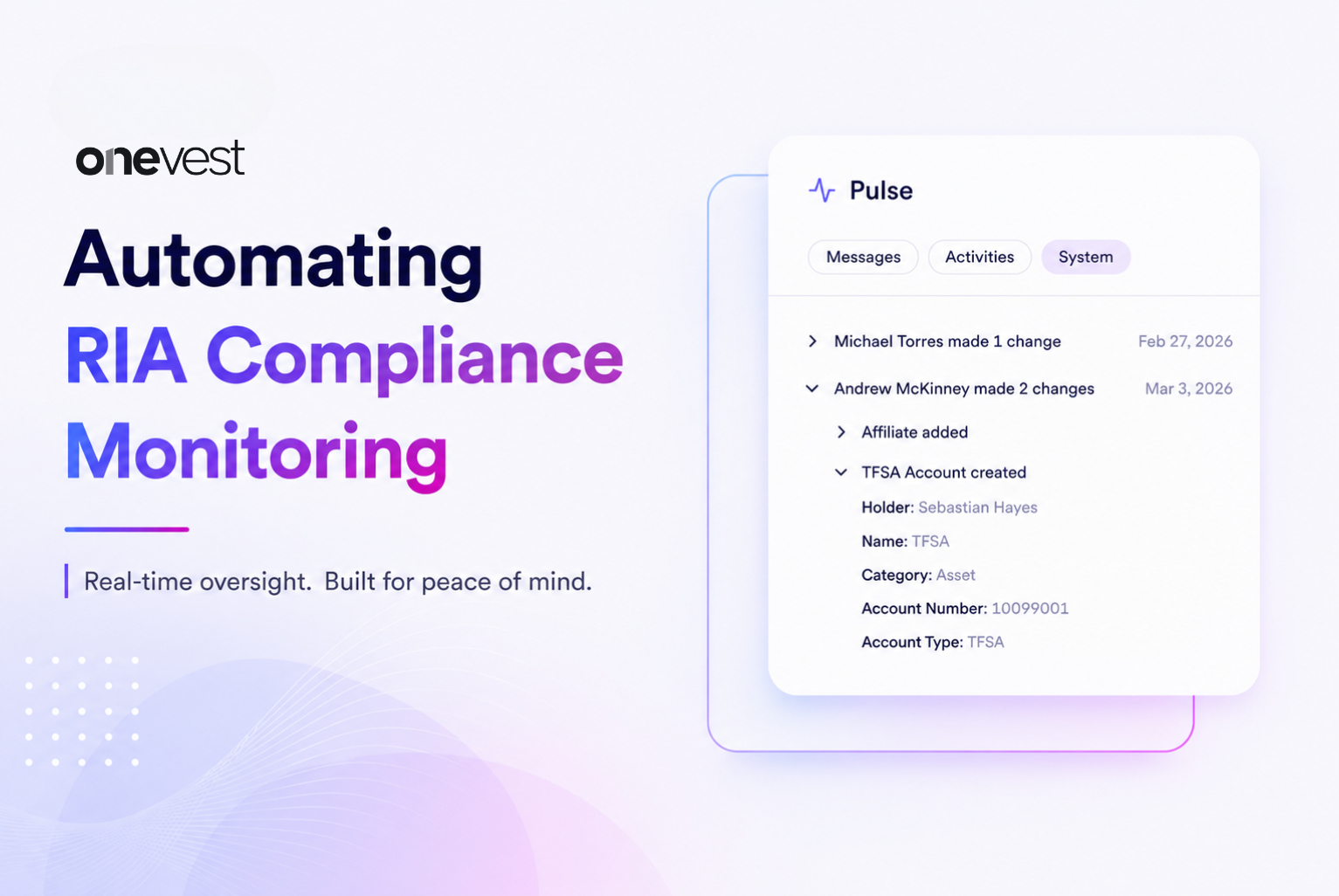

BlogAutomating RIA Compliance Monitoring: What Firms Need to Know in 2026

The SEC examination cycle is not getting quieter. In 2026, RIA compliance officers are managing more regulatory surface area, including heightened scrutiny of AI-driven investment tools, evolving…

Blog

BlogHow to Reduce Manual Wealth Management Operations: A Step-by-Step Guide

In 2026, wealth management firms that eliminate operational drag are unlocking faster growth, stronger compliance posture, and better client outcomes. The firms falling behind are not short on talent.

Blog

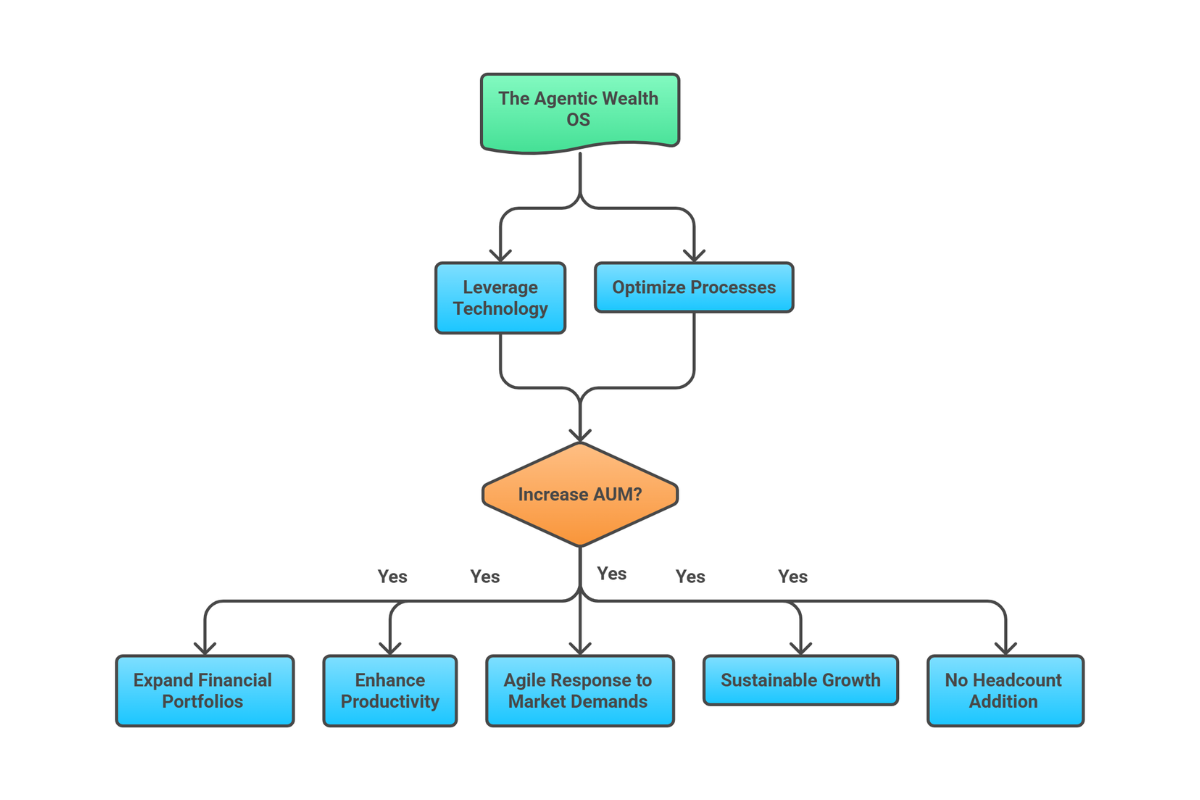

BlogThe Agentic Wealth OS: How Growing RIA Firms Are Scaling AUM Without Adding Operations Headcount

Agentic wealth management is reshaping how RIA firms grow. In 2026, the most competitive firms are not adding a back-office hire for every advisor they bring on.

Blog

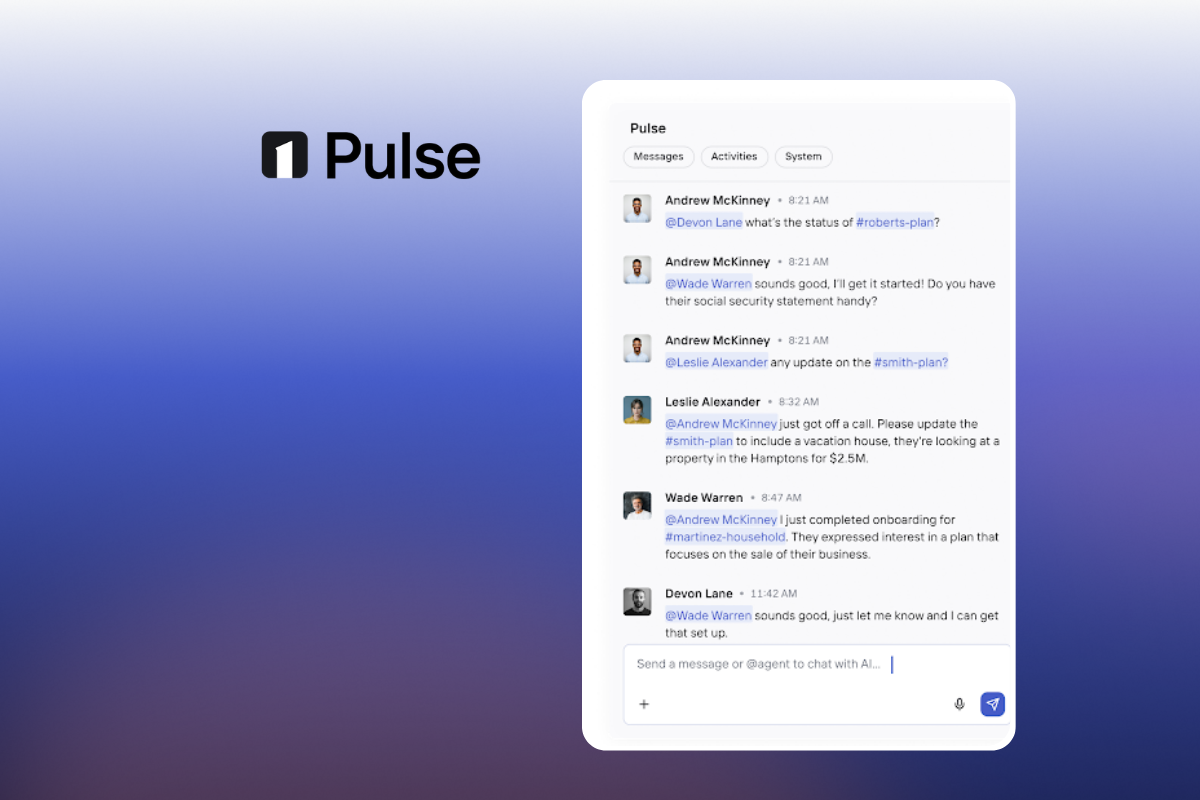

BlogOneVest Pulse: The Live Activity Stream Where Conversation Becomes Command

Fast-growing wealth management firms require solutions that can keep pace with the shifting operational needs of wealth management firms and their advisors.

Blog

BlogThe Investor-Led Revolution: How Client Expectations Are Redefining Wealth Management Software for RIAs

The strategic mandate for 2026 is clear: digital wealth management has become the primary interface of trust. In this AI-native era, the investor is now the primary architect of your technology…

Blog

BlogThe Top 7 Criteria for an AI-Native Wealth Management Platform: A Buyer’s Guide for Growing RIA Firms

Wealth management firms no longer compete solely on advice quality. They compete on experience, efficiency, and trust. Increasingly, those outcomes are shaped by the platform that runs the firm.

7 min Blog

BlogBuilt for Scale: How Customer Feedback Shaped OneVest’s 2025 Product Advancements

Over the past year, OneVest partnered closely with our customers, RIAs and enterprise wealth organizations to understand the day-to-day challenges that slow advisory teams down.

Blog

BlogAdvisor Onboarding in 2025: Why the Right Tech Stack Could Be Your Growth Engine

In today’s competitive RIA landscape, your technology stack can be the deciding factor between an advisor joining your firm, or your competitor’s.

5 mins min Blog

BlogAI in Action: Key Takeaways from Wealth Management EDGE 2025

This year’s Wealth Management EDGE conference made one thing clear, AI is no longer a future promise; it’s a present-day force transforming how wealth management firms operate, scale, and serve…

5 mins min Blog

BlogIndustry Outlook: Wealth Management Trends for 2025

As the year comes to a wrap, our thoughts pivot to what’s in store for the wealth management industry in 2025. One thing for sure is that change is the only constant.

5 mins min

See the Agentic Wealth OS in action.

Book a personalized demo and see how OneVest automates your workflows, unifies your team, and scales with your firm.